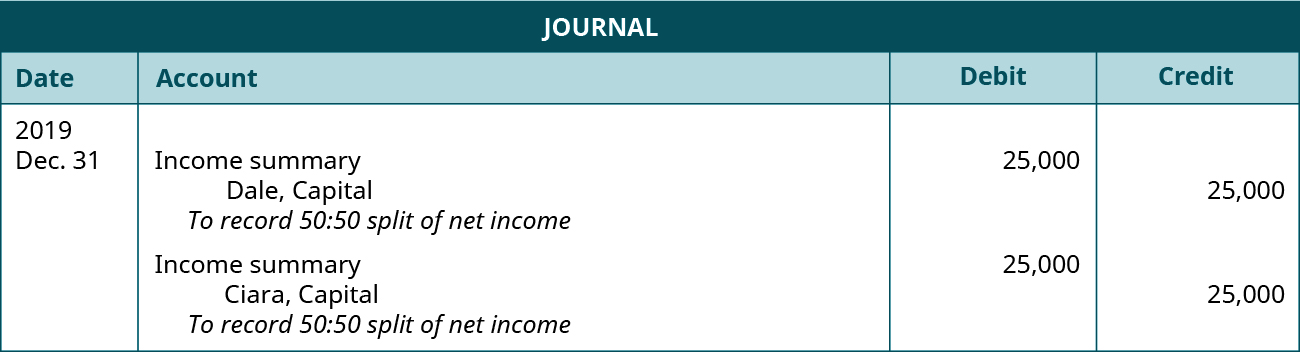

While writing down the mat credit entitlement following entry is to be passed.

Mat credit entitlement entry.

Mat credit entitlement account dr.

To profit and loss account b at the time of availment of mat credit.

Provision for taxation account dr.

To profit loss a c cr.

A tax credit scheme is introduced by which mat paid can be carried forward for set off against regular tax payable during the subsequent fifteen years period subject to certain conditions as under when a company pays tax under mat the tax credit earned by it shall be an amount which is the difference between the amount payable under mat and the normal tax.

Rs 14 43 000 rs 12 48 000 rs 1 95 000.

This is with effect from ay 2018 19 prior to which mat could be carried forward only for a period of 10 ays.

Mat credit is not a deferred tax asset as per as 22 on accounting for taxes on income issued by icai deferred tax liability or deferred tax asset arises on account of timing differences i e.

Whether mat credit being the deferred tax asset is decided to be carried forward further from financial year 2019 20 and onwards on the consideration that it is probable that future taxable profit will be available against which unused tax credits can be utilised.

The mat credit may however be shown separately as mat credit entitlement account.

The following entries are relevant in this context.

While availing the mat credit.

For this mat credit on 31st march the following entry is to be passed.

Provision for taxation a c dr.

Mat credit entitlement loans and advances dr 20 to mat expenses indirect expenses 20 summarizing the above situation the expenses debited to profit and loss will be rs 80 balance in mat expenses a c short term provisions shows mat payable of rs 100 loans and.

The following entry is to passed mat credit entitlement a c dr.

To mat credit entitlement.

Such tax credit shall be carried forward for 15 assessment years immediately succeeding the assessment year in which such credit has become allowable.

Thus mat credit can be understood as the difference between the tax calculated under the general provisions of the income tax act and that calculated under the mat provisions of the act.

The mat credit may be reflected as mat credit entitlement a c the following entry is to be passed for recognizing the mat.

Profit loss a c dr.

Such excess of tax credit is allowed to be carried forward and set off in the financial year in which the company is liable to pay tax under the general provisions of the income tax act.

The differences between taxable income and accounting income for a period that originate in one period and are capable of reversal in one or more subsequent periods.

Although mat credit is not a deferred tax asset under as 22 but it can be considered as an asset and the same should be presented under the head loans and advances considering it is of the nature of a pre paid tax.

Mat credit is utilised if income tax payable is more than mat so as per your question mat credit allowed in the earlier years but no entry is passed suppose for 2nd year provision for tax is 100 incometax mat is 80 mat credit entitlement a c has balance 20.